6 minute read posted by

6 minute read posted by Will your home keep rising in value? When’s the best time to sell in the next year? And how could moving help you with the cost of living? Here’s what the latest data from Zoopla’s House Price Index means for you.

Key takeaways

- Your home will continue to rise in value slowly over the rest of the year, totalling an average of 5% growth in 2022

- If you decide to sell, you’ll benefit from an average £19,800 rise in value in the past 12 months

- Downsizing or moving to an energy efficient home could help you offset interest rate rises and cost of living pressures

There’s a lot of noise around the UK housing market. And it can be hard to know when to stick, twist or make your dream move.

Richard Donnell, Director of Research and Insight, answers some of the most common questions about the UK housing market and how it will affect your home or move.

Will my home continue to rise in value this year?

We expect an average house price rise of 5% over 2022. Based on the average home, this translates to an extra £12,285 of value in that time.

So that’s a slowdown when you compare it to July 2021 to July 2022, when we’ve seen an average 8.3% (or £19,800) rise in house prices.

House prices are rising at different speeds right across the country and every market and street has its own local market.

The South West and Wales are jointly the best performing regions, with annual house price growth of 10.6%.

In terms of cities, Nottingham, Bournemouth, Leeds and Manchester lead the way with house price growth. They’ve all had 9% or higher price growth in the last 12 months.

While your house price growth will slow down, it’s more in line with the levels we see in a ‘normal’ market where prices tend to track growth in incomes.

By that, I mean if we take away the red hot market conditions we’ve all gotten used to since the pandemic.

Is there any chance my house price will fall?

While mortgage rates are set to double over 2022 we don’t anticipate any widespread falls in house prices.

While the rising rates and cost of living pressures are sure to be on households’ minds, we’re not seeing any big impacts on the market yet. The lasting effects of the pandemic are still a big influence on home moving decisions and house price growth.

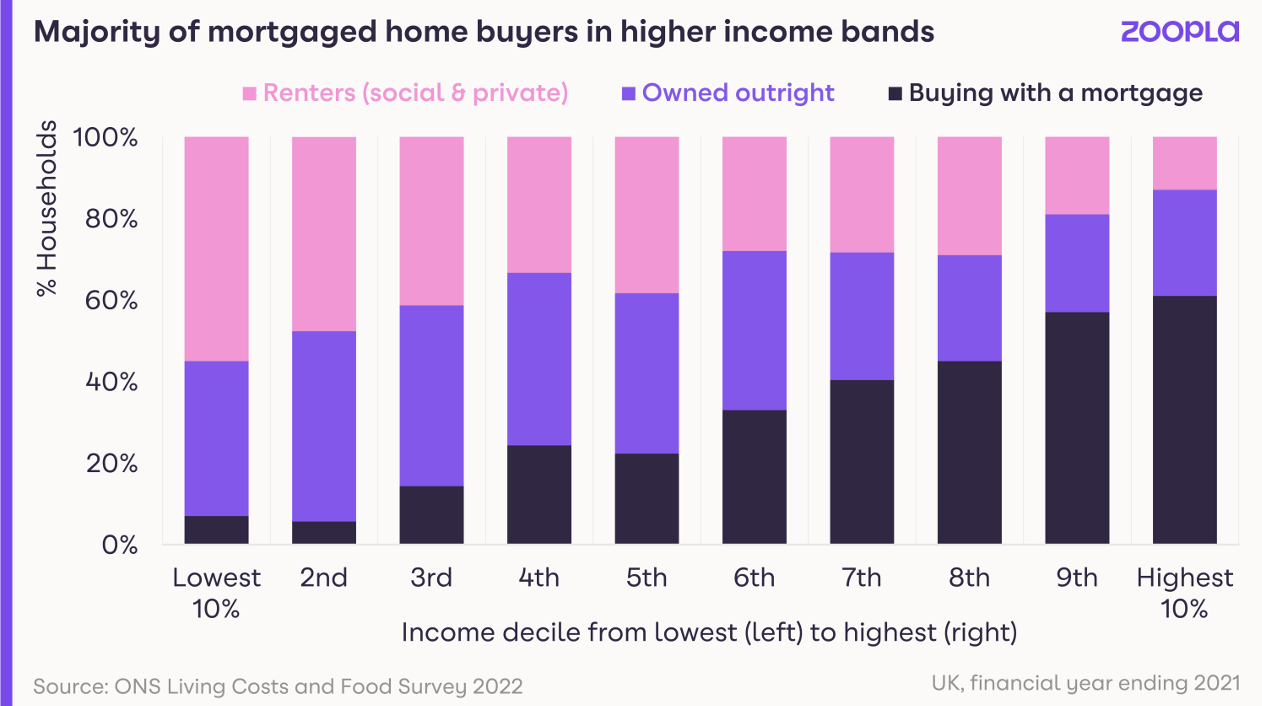

Home buyers with mortgages are proving more resilient than others to cost of living rises. The large majority of those buying with a mortgage, accounting for 7 in 10 of all new sales, sit within the middle to upper income bands.

The more mortgage rates increase above 4% then, we would be looking at zero house price growth over the following year.

We would only anticipate localised house price falls if mortgage rates were to rise higher than 5%.

With our data, we can usually foresee any falls in house prices, right down to individual postcodes. Stay in the loop by turning on email updates about your home and local market.

When is the best time to sell in the next year?

Moving house is a big decision. Most of us only do it once every 20 years.

I would put life changes and personal priorities before trying to time the market.

Don’t try to time buying decisions based on what you think will happen to house prices. There won’t be big swings in property values in 2023 but buyers will become more picky.

That puts you in a fairly strong position if you can weather cost of living rises and mortgage rate increases.

If you decide to sell, you’ll benefit from an average £19,800 rise in value in the past 12 months.

And right now, you’ll get more choice of your next home thanks to the seasonal uplift in homes for sale.

First time buyers and buy-to-let landlords are still very active at the moment. The average first time buyer price is £269,000, so homes valued around here can expect a strong demand from buyers with no chain.

The longer you wait to sell, you might see demand weaken as mortgage rates increase and the cost of living begins to bite.

However, you could find you’re in less competition when buying your next place as we head towards 2023. You may be more likely to have an offer accepted under asking price.

There’s no right or wrong time to buy or sell. It’s all about getting professional advice and weighing up the right choice for you.

How much interest should I expect to get in my home?

The interest you get will depend on the type of home you have, its size and its asking price – and how closely this is linked to what buyers in the area want to pay.

Typically, three bedroom semi-detached houses get the highest interest across the country. In London, it’s the two bedroom flat market that’s most in-demand.

But demand varies across the country depending on what’s happening in the local market. The best thing to do is follow similar properties for sale nearby.

We show you how long they’re on the market and even how many online views they get.

My other advice would be to talk to an agent long before you’re thinking of selling.

A good relationship with an agent is invaluable. They’ll know your local housing market better than anyone and can help you maximise interest in your home.

How could moving house help me with the cost of living?

Many of us are more conscious of what we’re spending, not just on mortgage costs but the overall cost of running a home.

We expect a higher proportion of households to consider downsizing to help with this.

Some will look to release equity, while others will look for a smaller or more energy efficient home.

New-build homes have much greater energy efficiency, so that might be one way to go. We recently found that a new-build home saves up to 52% on energy bills compared to a similar older property.

Or it might just be making sure your next home has a good EPC rating. The most common rating is D, but get closer to an A rating and you’ll save much more on utilities.

I’m a first time buyer. What can I do about rising interest rates?

First time buyers accounted for more than 1 in 3 sales so far this year and are an important group. Many are taking advantage of more flexible working to explore new markets seeking better value for money.

Even though mortgage rates are rising, the income to buy a typical first time buyer home in many areas is still the same as, or slightly cheaper than, renting.

Rising interest rates might make it more difficult for some first time buyers to get on the market.

But there are some options to help you offset the rise. The larger deposit you have, the better position you’ll be in.

Broaden your search area to more affordable markets, consider government schemes and do your research on the mortgage options available to you.

Spend plenty of time doing your research. Find a home that meets your needs and for which you feel you’re paying a fair price. Get advice about mortgage finance to help with this.

Source; Zoopla

by

by

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link